It's a common misconception that boat insurance is optional just because most states don't legally require it. The truth is, your actual boat insurance requirements are almost always set by private businesses. Think of it this way: you need car insurance to satisfy the law, but you also need it to get a loan or even park in some private garages. It's the same world on the water—you'll need specific coverage to dock at a marina or secure financing for your vessel.

So, let's cut through the noise. The real answer to "what boat insurance is required?" is a bit more involved than a simple yes or no. While a state government might not be knocking on your door, the practical side of owning a boat makes insurance pretty much non-negotiable. The real players setting the rules are your marina and your lender.

This system of requirements can feel a little tangled at first, but it really boils down to three simple questions: who is asking for coverage, what kind of coverage do they want, and what factors will shape your final price?

Who Sets the Rules?

For most boaters, the mandate for insurance comes from three main places, each with a very different reason for wanting you to have proof of coverage.

Let's break down who typically requires you to have boat insurance and what they're looking for. The table below gives a quick summary.

Who Requires Boat Insurance and Why

| Requiring Entity | Why They Require It | Typical Required Coverage |

|---|---|---|

| State Governments | To ensure financial responsibility for accidents on public waterways. | Liability Coverage (in states like Arkansas & Utah) |

| Marinas & Yacht Clubs | To protect their property and other members' boats from damage you might cause. | Liability Insurance, often with specific minimums. |

| Banks & Lenders | To protect their financial investment in your boat until the loan is fully paid. | Comprehensive & Collision Coverage. |

As you can see, state law is just one piece of the puzzle. The most common requirements you'll encounter will come from the private businesses you deal with as a boat owner.

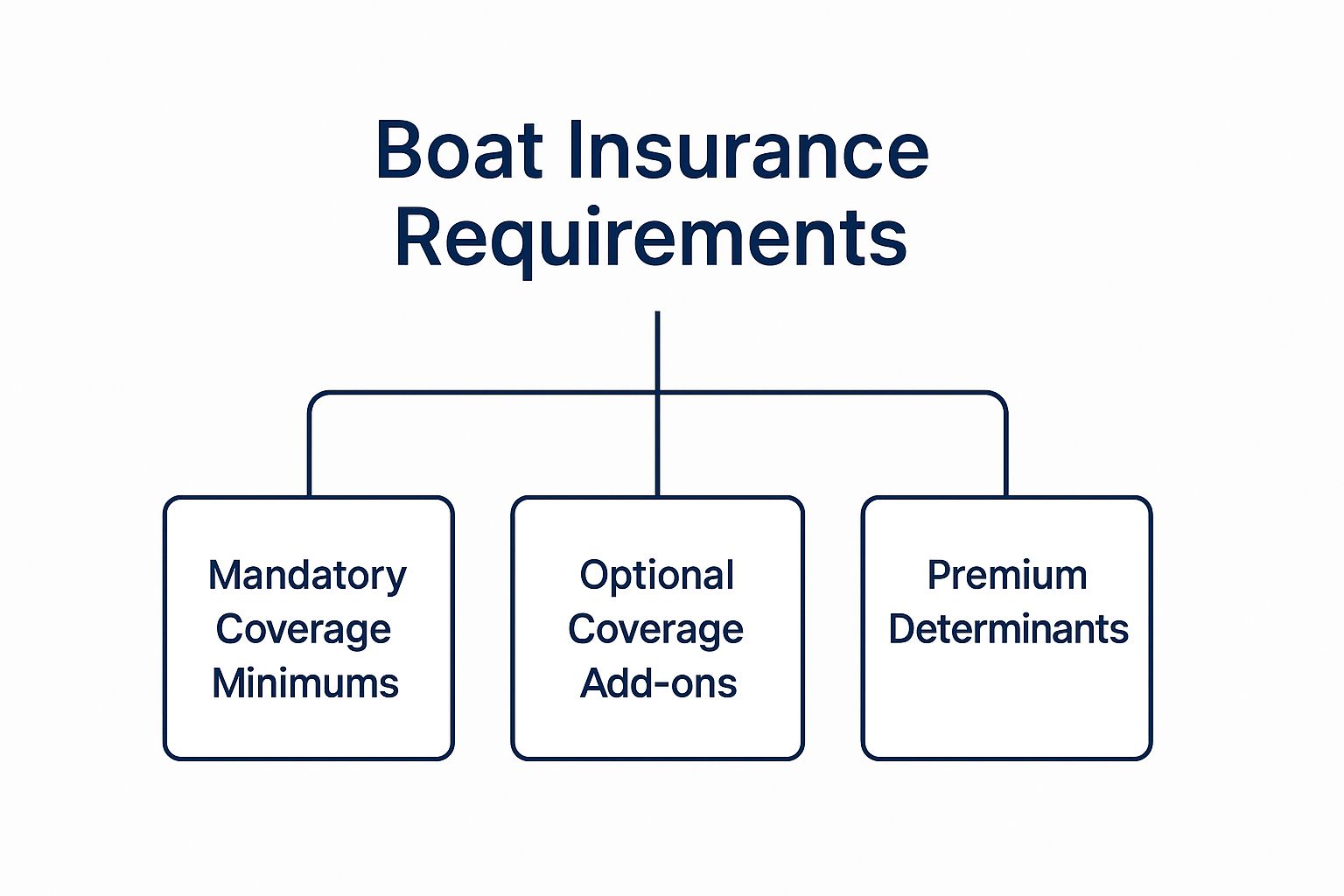

This image really helps visualize how your insurance needs are built, starting from the basic mandates.

Your mandatory coverage is just the foundation. From there, you'll add optional protections and see how different factors influence your premium, creating the final policy that's right for you.

The Growing Need for Protection

More boats are on the water than ever before, and with that comes a greater awareness of the risks involved. This has made insurance a central part of responsible, modern boating. You can see this trend reflected in the market itself; the global boat insurance market was valued at around $10 billion in 2023 and is expected to hit $15 billion by 2032. That’s a lot of growth, and it shows just how seriously owners are taking the protection of their valuable assets.

The most important thing to remember is that your insurance needs are unique to your situation. A boat kept on a trailer in your driveway has entirely different requirements than one financed and docked at a big commercial marina.

In the end, having the right insurance policy is just as critical as having the right safety gear. Good coverage provides financial peace of mind, while a well-stocked boat ensures everyone stays safe. For a full rundown of what you should have on board, take a look at our boating safety equipment checklist to stay safe on the water.

Decoding State and Federal Boating Laws

When you start thinking about boat insurance requirements, the first place most people look is the law. That makes sense, but what you find—or rather, what you don't find—can be misleading and create a false sense of security.

Here’s the first thing you need to know: there is no federal law that says you must have insurance for your recreational boat.

Think about car insurance. It’s required almost everywhere you drive on a public road. But for boating, the federal government steps back and lets individual states make their own rules. This means there isn't one single, nationwide regulation to follow. Your legal obligations are tied directly to where you register and use your boat.

This hands-off federal approach often leads boaters to assume insurance is just an optional extra. That's a huge mistake. While most states haven't passed specific insurance laws, a handful have, and you need to know who they are.

State-Specific Insurance Mandates

Only a couple of states have put laws on the books requiring boat owners to carry liability insurance. It’s absolutely critical to know if you live in one of these states—or plan to boat there—because ignoring the rules can lead to fines and even a suspended registration.

The two most common examples are Arkansas and Utah. They’ve set minimum liability coverage amounts to make sure boaters can cover the costs if they cause an accident.

- Arkansas: Here, you need at least $50,000 in liability coverage for any personal watercraft (like a Jet Ski) and any motorboat with an engine over 50 horsepower.

- Utah: This state requires all motorboats and PWCs to carry proof of liability insurance. The typical minimums are $25,000 for bodily injury to one person, $50,000 per accident, and $15,000 for property damage. Alternatively, a single combined policy of $65,000 works too.

And remember, even if your home state doesn't have an insurance mandate, you have to follow the rules of whatever state you're boating in. If you trailer your boat from a state with no requirements for a vacation on a lake in Utah, you better have that insurance policy ready.

Why No Law Doesn't Mean No Requirement

For the vast majority of boaters in states like Florida, Texas, or California where there's no legal mandate, it’s easy to think you’re off the hook. But the law is only one part of the story. The fact that a state doesn't force you to have insurance doesn't mean you can get by without it.

The most powerful insurance requirements almost always come from private businesses, not the government. A marina's demand for liability coverage often far exceeds any state-mandated minimum.

This is where the real world kicks in. Your marina will almost certainly demand proof of liability insurance before they let you tie up. They need to protect their docks, their property, and all the other boats moored there. If you financed your boat, your lender will also insist on a comprehensive policy to protect their investment.

In reality, these private requirements become the actual boat insurance requirements you have to meet. They are often much stricter than any state law. Understanding these rules is just as important as knowing the law, and it's a huge part of being a responsible boat owner. For more on this, check out our guide on the essential boating safety tips you should know to keep every trip safe and compliant.

The boating world is clearly moving toward greater responsibility. The entire marine insurance market is expected to grow from $32.31 billion in 2024 to $46.13 billion by 2032, a jump that shows just how many owners are seeking solid risk protection. You can discover more about marine insurance market trends on GlobeNewswire. At the end of the day, getting the right protection comes from understanding both the legal and the practical demands of boat ownership.

Why Marinas and Lenders Hold the Real Power

While very few states have laws on the books that force you to buy boat insurance, you'll quickly discover that the real rules are set by private businesses. When it comes to boating, your marina and your lender are the ones who truly call the shots on your insurance. They hold the keys to where you can dock and how you can pay for your vessel, giving them all the leverage.

Think of the marina manager as the gatekeeper. Their number one priority is protecting the marina itself—the docks, the facilities, and all the other boats moored there. To them, your uninsured boat is a huge, floating liability. A simple mistake while docking, an unexpected fire, or a fuel leak could trigger a chain reaction of damage, leaving them with a massive bill.

Because of this risk, it’s standard procedure for nearly every marina to have its own strict boat insurance requirements. These aren’t friendly suggestions; they're a non-negotiable part of your slip lease agreement. No proof of insurance, no slip. It’s that simple.

The Marina Mandate for Liability

So, what kind of coverage are marinas looking for? It all comes down to liability. They need solid proof that if your boat damages someone else's property, your insurance policy will step in to cover the costs. The limits they set are almost always far higher than any state minimums.

While the exact numbers can vary from one place to another, you can expect to see a few common demands:

- Minimum Liability Coverage: Most marinas will require at least $300,000 in liability coverage. Don't be surprised if more exclusive yacht clubs ask for $500,000 or even $1,000,000.

- Wreck Removal: If your boat sinks, getting it out of the water is a messy and surprisingly expensive job. This coverage handles that cost, so the marina doesn’t have to.

- Fuel Spill Liability: Marinas are on the hook for environmental compliance. This coverage ensures that if your boat leaks fuel or oil, the cleanup costs are covered.

By making every boater carry a solid liability policy, the marina creates a financially secure environment for everyone. It’s risk management 101: they're transferring the financial risk from their business and other boaters onto your insurance company. This is simply the cost of doing business.

Lenders Protecting Their Investment

If the marina is your gatekeeper, your lender is your co-owner. When a bank finances your boat, they have a major financial stake in it until you’ve paid off every last penny. Your boat is the collateral for their loan, and you better believe they’re going to protect that asset.

This is why any lender will insist you carry more than just liability. They’ll require you to have comprehensive physical damage coverage for the boat itself.

Lenders will typically mandate two specific types of coverage:

- Comprehensive Coverage: This protects the boat from just about anything other than a collision. Think theft, vandalism, fire, or storm damage. If your boat gets stolen, this is what protects the bank's investment.

- Collision Coverage: This pays to fix or replace your boat if you hit another vessel, a dock, a submerged rock, or anything else.

Your lender will also require you to name them as a "loss payee" on the policy. This is a crucial detail. It means that if your boat is totaled, the insurance payout goes directly to the bank first to settle your outstanding loan. This guarantees they recover their money before you see any of it. Without that safeguard, no lender would take the risk of financing such a valuable and mobile asset.

Choosing the Right Coverage for Your Boat

When you first dive into boat insurance, it can feel like trying to read a foreign language. The policies are full of jargon that can make your head spin. But trust me, getting a handle on these terms is the key to building a policy that actually has your back when you need it.

Meeting the minimum boat insurance requirements from your lender or marina is just the starting line. The real goal is to put together a plan that truly fits your life on the water. Think of it less like a single, rigid document and more like a set of shields. Each shield is designed to guard you against a different kind of risk, and you want to pick the right ones for the situations you're most likely to encounter.

The Three Core Protections

At the foundation of any solid boat insurance policy, you’ll find three main types of coverage. The names can sound a bit technical, but what they do is pretty simple. Let's break them down.

First, you have Liability Coverage. This is essentially your "oops" fund. If you’re at fault in an accident that damages another boat, a dock, or unfortunately, injures someone, this is what pays for the costs. It’s a firewall for your personal savings, covering legal fees and settlements so a mistake on the water doesn't sink you financially.

Next up is Hull Insurance. This is the boating world's version of collision and comprehensive auto insurance. It’s what pays to repair or replace your boat if it gets damaged, stolen, vandalized, or battered by a storm. Simply put, this coverage protects your biggest investment—the boat itself.

Finally, there’s Uninsured/Underinsured Watercraft Coverage. This one is huge. Picture this: another boater slams into you but has zero insurance, or their cheap policy won’t cover your repairs. This is where your own policy steps in to cover your boat and your medical bills. It ensures you don't get stuck with the tab for someone else’s mistake.

The real value of a great insurance policy isn't just checking a box—it's having the confidence that a bad day on the water won't turn into a financial catastrophe. The right combination of coverage provides true peace of mind.

To make this even clearer, this table breaks down how these coverages work in common scenarios you might face.

Comparing Essential Boat Insurance Coverages

This simple chart shows you exactly what each core coverage protects and gives you a real-world example of when you'd be glad you have it.

| Coverage Type | What It Protects | Real-World Example |

|---|---|---|

| Liability Coverage | Your assets from claims when you are at fault for property damage or bodily injury to others. | You accidentally collide with another boat while docking, damaging its side and injuring a passenger. |

| Hull Insurance | Your own boat from physical damage, theft, or total loss. | A severe storm causes a tree to fall on your boat while it's stored, crushing the cabin. |

| Uninsured Watercraft | You and your boat if you're hit by a boater with no insurance or insufficient coverage. | Another boater runs into you at a sandbar and flees the scene, leaving you with significant damage. |

Having these three pillars in place gives you a strong foundation, but now it's time to fine-tune your policy.

Tailoring Your Policy with Add-Ons

Once you have the core protections squared away, it’s time to customize your policy for how you actually use your boat. Standard policies have limitations, and that’s where endorsements—or add-ons—come in. These are small, specialized coverages that plug the gaps.

Think about adding some of these common options:

- Personal Effects Coverage: This covers all the stuff you bring aboard that isn't bolted down. We're talking about sunglasses, phones, coolers, and clothes that get damaged or stolen.

- Fishing Equipment Coverage: If you're a serious angler, you know your rods, reels, and tackle can be worth thousands. This protects that gear from theft or damage.

- On-Water Towing and Assistance: Breaking down on the water is a huge headache. This works just like roadside assistance for your car, covering the often-expensive cost of a tow back to shore.

- Towed Water Sports Coverage: Love to pull friends and family on a tube, wakeboard, or skis? That fun comes with extra risk. This endorsement gives you added liability protection specifically for those activities.

Picking the right add-ons is what turns a generic policy into one that feels like it was made just for you. It’s all about looking at your boating habits and making sure everything, from your expensive fish finder to your kids’ favorite tube, is protected.

How Your Boat and Habits Affect Your Rate

Knowing your state's boat insurance requirements is step one, but understanding what you'll actually pay is a whole different ball game. Think of your insurance premium as a custom recipe. Every single ingredient—from the type of boat you own to where you drop anchor—changes the final cost. Insurers are in the business of calculating risk, and they look at everything to figure out how likely you are to file a claim.

The boat itself is the star of the show. A high-performance speedboat will always cost more to insure than a simple fishing pontoon, for the same reason a sports car costs more to cover than a family sedan. More value and more power mean more potential for an expensive accident. Let's dig into the specifics that insurers really care about.

Your Boat's Profile

Every boat has its own unique risk profile, and insurers zoom in on these details to set your rate. Some factors have a much bigger impact than you might think, turning a seemingly small difference into a major change in your annual premium.

Here are the main things about your vessel that drive your insurance costs:

- Age and Condition: A brand-new boat might be pricey, but an older, poorly maintained one can be a huge red flag for an insurer. They see a higher risk of mechanical failure or even sinking. It's common for them to require a full marine survey on older boats to confirm they're still seaworthy.

- Boat Value: This one's simple. The more your boat is worth, the more it would cost to replace it. A $200,000 yacht will naturally have a higher premium than a $20,000 center console.

- Boat Length: Longer boats can cause more damage in a collision and often travel in more challenging waters. As a general rule, the longer the boat, the higher the insurance rate.

- Engine Horsepower: Speed is a massive risk factor in their eyes. A boat with a high-horsepower engine can get into trouble a lot faster than one with a small, quiet motor. This bumps up the cost for both liability and hull coverage.

Regular maintenance is key, and insurers love to see you're proactive. For example, actively combating saltwater corrosion in marine vessels shows you’re serious about protecting your investment, which can positively influence your rate.

Where You Boat Matters

Your stomping grounds are just as important as the boat itself. An underwriter will look very differently at a vessel used only on a small, calm inland lake compared to one that regularly cruises the unpredictable open ocean.

Think of it like this: driving in a quiet suburban cul-de-sac is far less risky than commuting through downtown Manhattan during rush hour. The same principle applies to your boating location.

Coastal boating automatically comes with higher risks like hurricanes, saltwater damage, and crowded shipping lanes—all things that push premiums up. On the flip side, sticking to a freshwater, landlocked lake is generally seen as safer and, therefore, cheaper to insure.

The Captain's Record

Finally, insurers take a hard look at the person at the helm: you. Your personal history gives them a good idea of how responsible you are, which they use to predict your chances of filing a claim.

Several personal factors come into play:

- Your Boating Experience: A captain with decades of experience under their belt is viewed much more favorably than a brand-new boater. More time on the water suggests better skills and judgment.

- Your Claims History: If you have a history of filing boat insurance claims, you can bet you'll pay more. A clean record speaks for itself.

- Boater Safety Courses: This is one of the easiest ways to get a discount. Completing a recognized boater safety course proves you're committed to safety and often earns you a discount of 5% to 10%.

- Your Credit Score: In many states, insurers use a credit-based insurance score as part of their calculation. A strong credit history can often lead to lower premiums.

Once you understand these moving parts, you can take control. By taking a safety course, keeping up with maintenance, and boating responsibly, you can actively lower your risk profile and your insurance bill.

Frequently Asked Questions About Boat Insurance

It’s completely normal to have a few questions when you start digging into the details of boat insurance. Let's clear up some of the most common ones so you can feel confident you've got the right coverage.

Will My Homeowners Insurance Cover My Boat?

This is a question I hear all the time, and the short answer is almost always no. A standard homeowner's policy might offer a tiny bit of property coverage—usually around $1,000 to $1,500—but that's only for a small, non-motorized boat like a canoe or kayak, and typically only while it's stored at your home.

The second that boat hits the water, that minimal coverage often vanishes. More importantly, your homeowner's policy provides absolutely zero liability protection for boating incidents. For any vessel with a motor or real value, a dedicated boat insurance policy is the only way to get the protection you actually need.

Do I Need Separate Insurance for My Jet Ski?

Yes, you almost certainly do. Personal watercraft (PWC) like Jet Skis and Sea-Doos are powerful machines, and they need their own specific policy.

In states like Utah and Arkansas where boat insurance is mandatory, PWCs are almost always included in the law. Even where it’s not required by the state, your marina or storage facility will demand proof of liability coverage before they let you on their property. Think about it: because of their speed and agility, PWCs come with a unique set of risks, making a PWC-specific policy a must-have.

It's a good rule of thumb: if it has a motor and you use it on the water, it needs its own insurance policy. Never assume your main boat policy will automatically cover a PWC you add to your fleet later.

What Happens If I Boat Without Required Insurance?

Skipping out on required insurance is a gamble you don’t want to take. The consequences can be severe, hitting your wallet hard and potentially sidelining you from boating altogether. The fallout really depends on whose rules you're breaking.

Let's break down the potential trouble:

- From the State: If you’re boating in a state with an insurance mandate and you get caught without it, you can expect hefty fines. They could also suspend your boat’s registration, which means you can’t legally use it on public waters until the issue is resolved.

- From Your Marina: Marinas don’t mess around with their insurance rules. They can—and will—terminate your slip agreement and give you a deadline to remove your boat from their property.

- From Your Lender: If you have a boat loan, your agreement requires you to maintain insurance. If you let it lapse, your lender might repossess the boat or buy a very expensive "force-placed" policy on your behalf and tack the huge premium onto your loan.

- From an Accident: This is the nightmare scenario. If you cause an accident without insurance, you are on the hook for every penny of property damage and medical bills. A single incident could lead to crippling lawsuits and financial devastation.

Staying properly insured is a fundamental part of responsible boat ownership. It's just as vital as knowing the rules of the water and keeping the right safety gear on board. To make sure you're ready for every trip, take a look at your ultimate safe boating checklist.

End fueling frustrations for good. With the spill-proof system from CLiX Fueling Solutions, you can refuel with confidence, knowing you'll never overfill your tank again. Protect your boat, the environment, and your peace of mind by visiting https://clixfueling.com to get yours today.